Minnesota's marketplace enrollment uses a state-run exchange called MNsure.

MNsure is a place where people can purchase individual/family health insurance, and receive premium subsidies and cost-sharing subsidies if eligible. This is a valuable service for people who are not eligible for Medicare or employed by a company that provides group health insurance.

Minnesota residents can also enroll in MinnesotaCare (the state's Basic Health Program) through MNsure. Medicaid enrollment can also be done through MNsure, although enrollment in some types of Medicaid (for the elderly, disabled, etc.) is done through the state's Medicaid office.

In 2017, state lawmakers voted to convert MNSure to a federally run marketplace, but the legislation was vetoed by then-Governor Mark Dayton. This issue came up again in 2021, but the legislation did not advance.

Read more about the history of Minnesota's health insurance marketplace.

The open enrollment period for 2022 coverage ran from November 1, 2021 to January 15, 2022. Outside of open enrollment, a qualifying event is necessary to enroll or make changes to your coverage.

There are five insurers that offer exchange plans in Minnesota. Quartz was new for 2021, and all five insurers have continued to offer coverage for 2022. Most counties in Minnesota have at least three insurers offering exchange plans for 2022, although there are seven counties that have just two insurers that offer plans through MNsure.

The following insurers offer plans in the Minnesota exchange, with plan availability varying from one location to another:

- Blue Plus

- Group Health

- Medica

- UCare

- Quartz

PreferredOne also offers individual/family coverage in Minnesota, but only outside the exchange (ie, their plans are not available through MNsure).

For 2022, Minnesota's individual-market insurers implemented an overall average rate increase of 9.5%, due in part to changes to the state's reinsurance program.

But that average rate increase applies to full-price plans. The majority of MNsure enrollees receive premium tax credits (subsidies) that offset some of the cost. And subsidies grow to keep pace with changes in the benchmark plan (second-lowest-cost Silver plan) in each area. The American Rescue Plan has made the subsidies larger and more widely available than they were in the past, and that continues to be the case for 2022.

Minnesota's exchange enrollment dropped for the first time in 2019, when 113,552 people enrolled in individual market plans through MNsure. But it climbed again, to 117,520, during the open enrollment period for 2020 coverage, and to 122,269 people who enrolled during the open enrollment period for 2021 coverage.

During MNsure's COVID-related enrollment window in 2021, nearly 12,700 people had signed up for coverage by July 12 (the window continued through July 16).

In the first two weeks of the open enrollment period for 2022 coverage, new enrollments via MNsure (as opposed to renewals) were up 21% over the previous year.

Read more about Minnesota's health marketplace.

Minnesota has enjoyed a low uninsured rate for years due to generous Medicaid eligibility standards and MinnesotaCare, a health insurance program for uninsured, working residents. Under the Affordable Care Act, Minnesota not only expanded Medicaid, it also created a state-based health insurance exchange called MNsure.

As of the first half of 2020, there were nearly 107,000 people with private individual market coverage through MNsure. All of them have coverage for the ACA's essential health benefits with no lifetime or annual caps on the benefits. And more than 59,000 of them were receiving premium subsidies that make health insurance more affordable.

According to U.S. Census data, Minnesota's uninsured rate fell from 8.2 percent in 2013 to 4.1% in 2016. But it increased slightly, to 4.4% as of 2018, and increased again, to 4.9%, as of 2019. That uptick in the uninsured rate was common across the country after the Trump administration took office. It was due in part to new federal policies that undercut the ACA, but also to rising health insurance premiums — themselves due in part to Trump administration and GOP congressional actions — that made coverage less affordable for people who don't qualify for premium subsidies.

In the 2010 passage of the Affordable Care Act, Minnesota's two Democratic senators – Amy Klobuchar and Al Franken – both voted in support of health reform. Franken is credited for the inclusion of a medical loss ratio (MLR) requirement in the reform bill, which has resulted in marketplace insurers sending rebates — often substantial ones — to enrollees when the percentage of collected premiums spent on enrollees' medical bills is below the allowable minimum.

One of the early, popular provisions of the ACA, MLR requires insurance companies to issue refunds if they spend more than 20% of premiums on administrative items (15% for large-group plans). The MLR rule resulted in $1.1 billion in refunds in 2012, and by the end of 2019, total cumulative refunds had reached more than $5 billion.

Franken resigned in 2017, and Minnesota's Lieutenant Governor, Tina Smith, was appointed to fill his spot in the Senate. Smith then won the special election for the seat in 2018. Klobuchar also won her re-election bid in 2018, so both of Minnesota's Senators continue to be Democrats.

Minnesota's eight representatives split their votes on the ACA in 2009/2010, with Democrat Collin Peterson joining three Republicans in voting no. Peterson did not support 2017 House Republicans in their efforts to pass the American Health Care Act, a partial ACA repeal bill, but his votes on health care reform were a mixed bag over the years. After 15 terms in office, Peterson was replaced in 2021 by GOP Representative Michelle Fischbach, who is opposed to the ACA.

Minnesota's U.S. House delegation consists of four Republicans and four Democrats in 2021. Four districts (1st, 2nd, 3rd, and 8th) flipped in the 2018 election, but two flipped to the Democrats and two flipped to the Republicans. And the 7th district flipped from Peterson (a conservative Democrat) to Fischbach (a Republican) in the 2020 election.

Minnesota's former governor, Mark Dayton, had long been a proponent of Obamacare. Dayton chose not to run for a third term in 2018, but Tim Walz, the DFL (Democratic-Farmer-Labor) candidate, won the election, so the governor's seat continues to be occupied by a Democrat.

After Democrats gained control of Minnesota's House and Senate in the 2012 election, legislation was passed to implement a state-run health insurance exchange. Minnesota also expanded Medicaid, which it calls Medical Assistance, to residents with household incomes up to 138 percent of the federal poverty level. Medicaid expansion was a key ACA strategy to reduce the uninsured rate. And as noted above, Minnesota also created a Basic Health Program under the Affordable Care Act, further protecting residents with income a little above the Medicaid eligibility cut-off.

In February 2013, Governor Mark Dayton signed HF9, a bill that expanded access to Minnesota's Medicaid program under the ACA. From late 2013 to May 2021, enrollment in Minnesota Medicaid plans (Medical Assistance) and CHIP plans increased by 39%. During the Covid-19 pandemic, enrollment in Minnesota's managed Medicaid plans surged nearly 17% from February through October 2020.

Minnesota also established a Basic Health Program (BHP) under the ACA, and is one of only two states to do so (New York is the other). Basic Health Programs provide robust, low-premium coverage to people with income between the Medicaid eligibility threshold and 200% of the poverty level, as well as to legally present non-citizens with incomes below 138% FPL who are time-barred from enrolling in Medicaid. In Minnesota, the Basic Health Program is known as MinnesotaCare, a program that predates the ACA but was revamped to serve as a BHP as of January 2015.

(New York also created a BHP as of 2016; to date, New York and Minnesota are the only states that have BHPs, although DC's Medicaid eligibility extends to 210% of the poverty level.)

Premiums and out-of-pocket costs in MinnesotaCare are lower than in plans offered at low incomes in other ACA marketplaces. At various points Minnesota lawmakers have considered extending access to MinnesotaCare to higher income levels or even all income levels, but such plans have not been enacted.

Read more about Minnesota's Medicaid expansion.

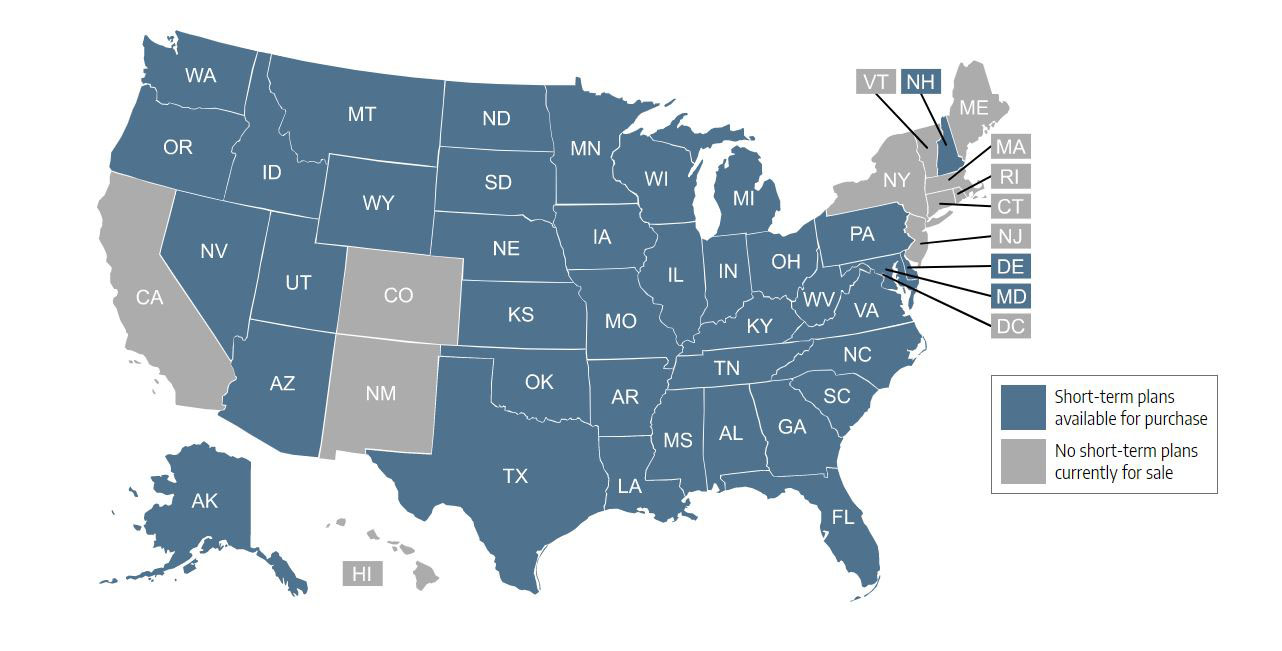

Short-term health insurance plans in Minnesota cannot last more than 185 days unless the insured is in the hospital on the day that the plan would have terminated and the insurer extends the coverage until the end of the hospital stay.

Short-term plans are nonrenewable in Minnesota, but a person can buy additional plans as long as their total time with short-term coverage doesn't exceed 365 days out of any 555-day period – plus any days that a plan is extended to cover an insured who is in the hospital on the day the plan would have ended. Buying a new plan entails starting over with a new deductible.

Read more about short-term health insurance coverage in Minnesota.

By September 2021, there were 1,070,620 people enrolled in Medicare in Minnesota.

Minnesotans can choose Medicare Advantage plans instead of Original Medicare if they wish to obtain additional benefits and don't mind the restrictions (including network restrictions) that go along with having a private plan. Nationwide, about 43% of Medicare beneficiaries are enrolled in private plans, but in Minnesota, it's nearly 53%. Most of these enrollees have Medicare Advantage plans, but some have Medicare Cost plans, a form of commercial Medicare coverage that pre-dates Medicare Advantage. Minnesota has long had the nation's highest enrollment in Medicare Cost plans, but about 300,000 enrollees had to switch to different coverage (Original Medicare or Medicare Advantage) when their Cost plans were phased out in 2019.

Read more about Medicare in Minnesota, including details related to Medigap plans and Medicare Part D.

- MNsure – the state's health insurance marketplace, and the only place Minnesota residents can obtain financial assistance with the cost of their individual health insurance premiums.

- Greater Minnesota Healthcare Coalition

- Minnesota Department of Human Services, Health Care Coverage – Medicare Assistance (Medicaid)

- Minnesota State Health Insurance Assistance Program – Information and resources for Minnesota Medicare beneficiaries

Before the ACA reformed the individual health insurance market, coverage was underwritten in nearly every state, including Minnesota. As a result, people with pre-existing conditions were often unable to purchase coverage in the private market, or if coverage was available it came with a higher premium or with pre-existing condition exclusion riders.

The Minnesota Comprehensive Health Association (MCHA) was created in 1976 to give people an alternative if they were ineligible to purchase individual health insurance because of their medical history. (Only Connecticut has a risk pool as old as Minnesota.)

Under the ACA, all new health insurance policies became guaranteed-issue starting on January 1, 2014. This change largely eliminated the need for high-risk pools and MCHA stopped enrolling new members as of December 31, 2013. It remained operational for existing members until the end of 2014.

0 Response to "Is Minnesota Continuing Health Insurance Assistance in 2018"

Post a Comment